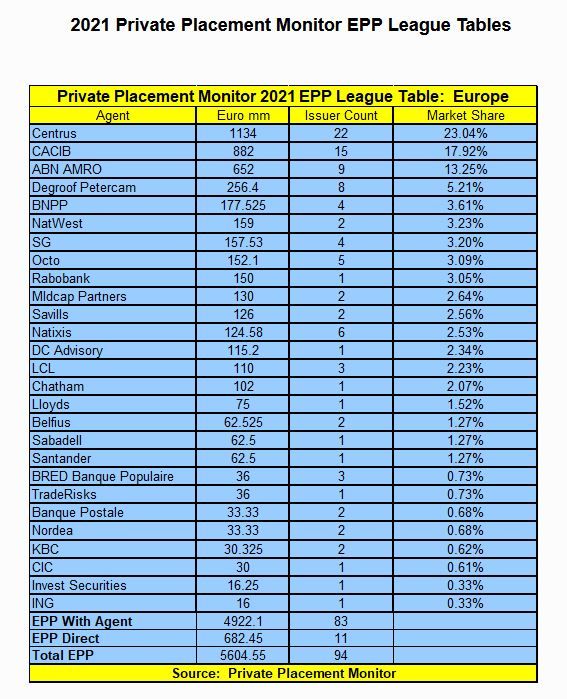

We are pleased to announce that Centrus has been ranked #1 on the Private Placement Monitor European Private Placement League Table by both deal count and volume for 2021.

To learn more about our work in this area with clients including London School of Economics, South Staffordshire PlC, Henderson European Focus Trust and Melin, click here.

For more information, please contact Maria Goroh, Senior Director – Centrus

Back in 2014, Centrus worked with Cross Key Homes to secure the first Housing Association issued ‘Green Bond’. Since then, we have been pleasantly surprised at the rapid adoption of Environmental, Social and Governance (ESG) accredited and labelled financing in the market. Between early 2020 and mid 2021, the housing sector moved from nearly 100% non-labelled issuance to 100% ESG labelled issuance.

While it is not yet a prerequisite for funding, ESG has become increasingly baked into the ecosystem, both for issuers building this into their reporting standards, as well as on the lender and investor side of the equation where it’s becoming fundamental to the credit process.

At this year’s NHF Housing Finance Conference Centrus Co-founder, Phil Jenkins and Director Lawrence Gill addressed the impact of ESG on the funding landscape. Centrus were joined by Anne Costain, Executive Director of Finance at Stonewater, Brenden Sarsfield Chief Executive Office at Sustainability for Housing and Imran Mubeen, Head of Treasury at Bromford Housing Group.

Here are three key takeaways from their discussion:

1. The Rise of ESG Reporting

The most immediate trend has been the rapid adoption of the Sustainability Reporting Standard (SRS). Launched in 2020, the SRS is a voluntary reporting framework, covering 48 criteria across ESG considerations such as zero carbon targets, affordability, safety and resident voice. With over 100 organisations signed up already, the sector has made a great start in adopting ESG reporting, which many believe will become mandatory in the future.

The SRS allows housing providers to report their ESG performance in a transparent, clear and comparable way. Not only does this differentiate the issuer from their competitors, but makes it easier for lenders and investors to assess ESG performance, risks and pursue opportunities.

Beyond the SRS, the next step could be to consider impact reports from an accredited third party. This will allow HAs to quantify how much benefit their actions bring and demonstrate with more clarity how they are generating positive change for otherwise underserved stakeholders.

2. The move towards Sustainability-Linked Bonds in the Housing Sector

While a Sustainability Bond, otherwise known as a ‘use of proceeds bond’, involves proceeds being allocated to projects which further the UN’s Sustainability Development Goals (SDGs), a Sustainability-Linked Bond (SLB) has Key Performance Indicators (KPIs) embedded within it. These are specific social and environmental targets aligned both to your sustainability strategy and the SDGs.

Earlier this year, L&Q successfully completed the first Sustainability-Linked Bond in the housing sector. The £300m issue directly linked to the housing association achieving a set of targets around reducing operational carbon emissions, improving the energy efficiency of residents’ homes, and delivering new affordable homes.

As Housing Associations are in intrinsically tied to ESG due to their responsibilities within communities in which they work, this is a clear next step for the sector.

3. More ambitious KPIs and goals

As the use of ESG labelled finance and SLBs become more widely adopted, and the sector inevitably opens itself up to criticism and accusations of greenwashing, the next challenge will be to ensure that these KPIs are set appropriately, transparently and that targets are sufficiently ambitious.

Targets should be about additionality – delivering benefits over and above the borrower’s business-as-usual strategy.

Relevant to the issuer’s overall business, and of high strategic significance to the issuer’s current and/or future operations

Measurable or quantifiable on a consistent methodological basis

Externally Verifiable, and

Able to be benchmarked, as much as possible using an external reference or definitions to facilitate the assessment of the organisation’s level of ambition.

Please get in touch with a member of our team for more information.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you agree to our Privacy Policy

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.