Rising insurance premiums

Since 2020, insurance premiums have increased substantially, putting further pressure on operating margins for the sector.

A combination of fire safety, weather-related risks, inflation in reinstatement costs and some insurers getting cold feet has resulted in a very different insurance market today.

The insurance industry is putting a greater emphasis on risk exposure, which is subjective.

Loss ratios, which are factual and backward-looking, are probably a source of frustration for the sector given the rate of increase in insurance premiums.

A bit like pricing the risk of default on a loan, pricing the risk of a weather-related event involves a huge amount of data, an interlinked financial system and a degree of judgement.

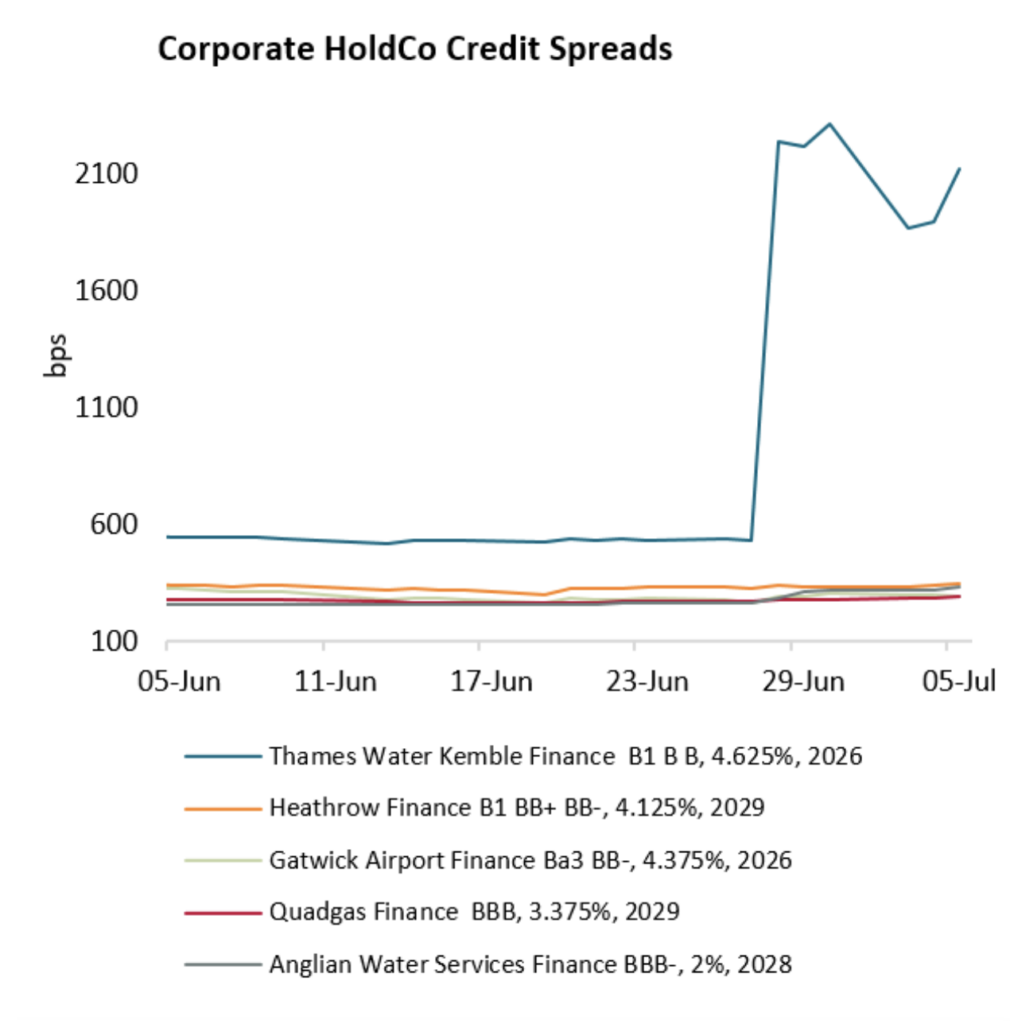

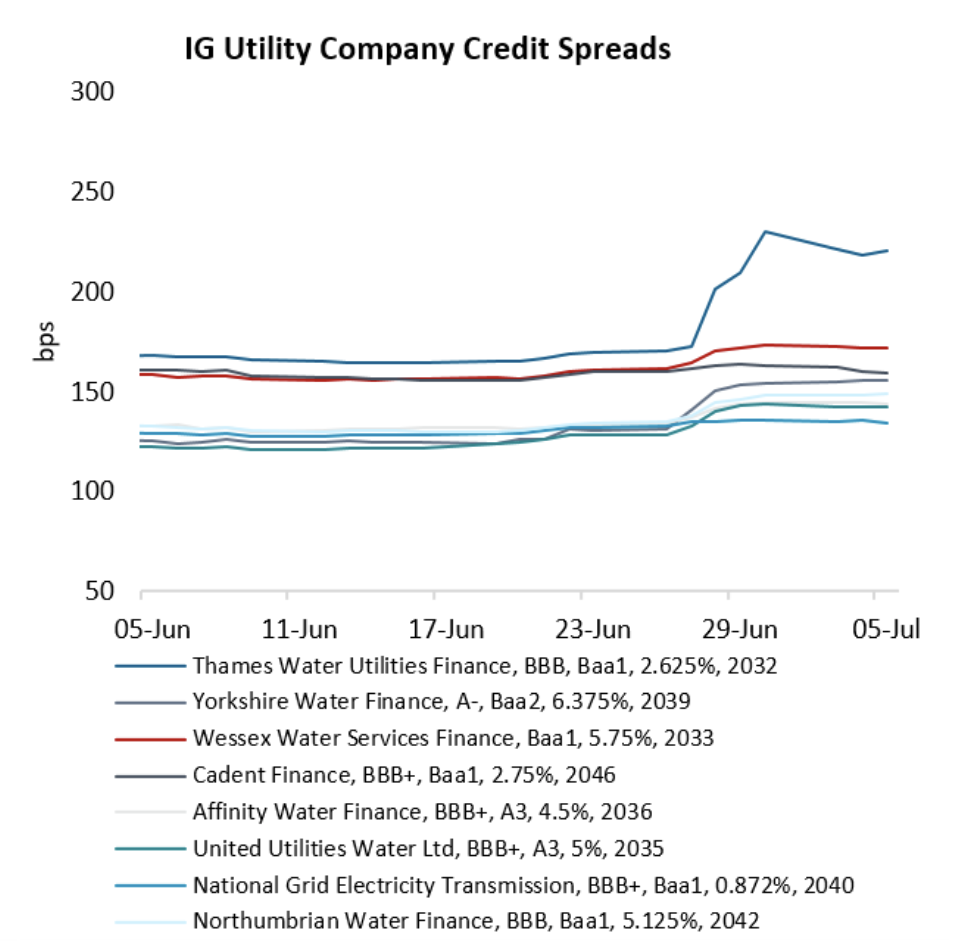

After the financial crisis, the risk premium paid for capital increased substantially but normalised in about a year.

Despite a recent ‘once in a 100 years’ pandemic and a cost of living crisis, risk premium on debt or credit spread is currently relatively low by historic standards.

However, the price of re-insurance is probably going to stay high for the foreseeable future due to a more volatile global climate.

What can RPs do to keep the price of insurance under control?

Some of the largest RPs in England have strong enough balance sheets to explore the possibility of a captive insurance agent, which are insurance companies within a group that access the re-insurance market directly.

The credit strength of some RPs could in theory lead to attractive pricing. However, given the legal and regulatory complexity, it is understandably very rare in the sector.

Increased excess amounts or partially self-insuring up to a set level is the most obvious option.

Full self-insurance, which involves setting aside funds to cover potential losses instead of purchasing insurance coverage, is not a particularly attractive option for a risk-averse sector with a long track record of raising capital and no defaults.

Lenders typically require RPs to maintain insurance on charged stock ‘that is usual for RPs and whose practice is not to self-insure’.

Where higher excess levels sit within the definition of ‘usual for RPs’ is an interesting question.

If borrowers take significant action to reduce insurance premiums by rebalancing risk, lenders may seek to adjust their approach to loan security or request detailed risk assessments and mitigation plans.

The importance of quality stock data and information knows no bounds.

At a time when business plans are stretched and headroom on loan covenants is low by historic standards, introducing elements of self-insurance or a potential and material one-off cost of insurance excess needs some careful thought.

How much headroom would be eroded? How much time would there be to react? What is the potential liquidity impact? Is there a reputational risk with other stakeholders?

There may be a way for RPs to collaborate to either pool risk or combine credit strength to reduce the cost of insurance.

However, this is a highly complex proposition with varying degrees of risk and risk management across RPs.

A specialist insurer with a different way of underwriting the risk for the difficult pockets of stock is probably the best alternative to explore if conventional insurance solutions are not economic.

Web 3.0 and blockchain technology could reduce insurance premiums in the future by enabling the creation of smart contracts, streamlining through decentralised insurance platforms, and improving risk assessment through big data.

While RPs wait in hope for this potential revolution, they will want to tread carefully and consider the potential treasury impact of any options being considered.

Originally published in Social Housing Magazine