The Centrus team is very pleased to be joining the growing City Giving Day group of supporting companies in September this year. Centrus Communities is a precious part of our company culture and working with inspiring charities reflects our core ambition to provide modern finance with purpose. If your company would also like to join, please follow this link to register: www.lordmayorsappeal.org/cgd

We had the chance to answer the Lor Mayor’s Appeal questiosn about why we are joining and what it means to us on the CITY AM 10 July 2019 edition.

Why are you supporting CGD?

Centrus Communities is a precious part of our company culture driving a good range of community initiatives. These are inspiring charities that work in the same sectors as our financial experts. The organisational and profile support from City Giving Day gives huge momentum to the internal and external awareness of these contributions.

It also adds further opportunities for action, whether with our time, donations or professional input.

Which charities do you support?

We focus on charities, specific projects or social enterprises within our sectors of work such as the housing sector. We offer probono support to these projects and social enterprises, for example structuring, financial modelling or business planning as well as volunteering employee and partner time across a range of activities.

How will you celebrate CGD?

We are signed up to the Tour de City, always relishing a challenge! It is also part of the fund raising and training for our May 2020 ‘Cycle with Purpose’ event in which we are riding between our London and Dublin offices. We will all be celebrating by supporting the Lord Mayor’s Appeal through dressing ourselves and our office in Red for the day.

Charity in action

We are supporting the Single Homeless Project (SHP) and the Lord Mayor’s Appeal. SHP is a London-wide charity working to prevent homelessness and help vulnerable and socially excluded people to transform their lives.

“Working with inspiring charities reflects our core ambition to provide modern finance with purpose. Being part of the City Giving Day further encourages this inspiration to bring out the best in our people and teams.”

George Roffey, Head of People, Culture and Brand said

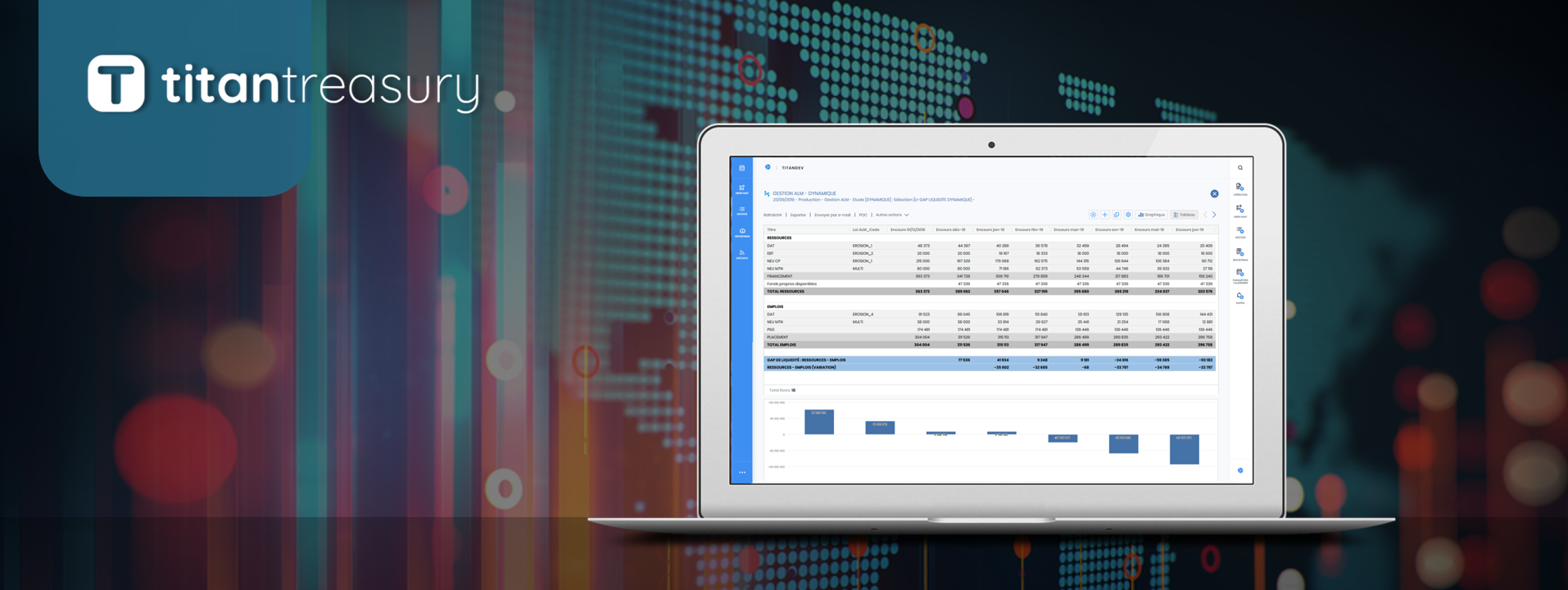

These are the five reasons why titan treasury is in Deloitte’s top 8 TMS solutions: delivery model, deployment time, frequency of updates, functionalities, but most importantly… because of it’s focus on people.

The Centrus Analytics and 3V Finance teams are very pleased to see that, after a few months of interviews and detailed answers to an extensive Request for Proposal (RFP), titantreasury has made it to Deloitte’s list of 8 leading Treasury Management Systems available to the UK market.

The Deloitte Treasury Technology Market Intelligence 2019 report, published this May, aims to help businesses map out their treasury strategy and requirements in order to find the best treasury management system vendor to match these needs and beyond.

The report is a market based review of today’s and tomorrow’s Treasury technologies and how their implementation, which could be seen as a challenge to most organisations, can actually be an opportunityto deploy creative solutions that deliver simple, transparent and efficient Treasury processes.

The report maps out the current Treasury Management System’s vendor market. Deloitte has surveyed 8 leading vendors, covering 14 individual systems, based on what the consultancy firm has observed most often amongst their clients.

The key comparison criteria between vendors were (1) delivery model, the (2) average deployment time, the (3) frequency of major platform upgrades and the (4) level of functionality coverage.

See below how titantreasury performed in each of these criteria:

1.Delivery model

titantreasury gives the users the delivery options to choose from that best suits their organisational needs.

2. Average deployment time

Disciplined communications, close project management and exceeding client expectations are key to sucessfully delivering a software between 3 to 5 months on average. We have pushed the limits on this by bringing our average implementation time in 2019 to less than 2 months. A detailed kick-off phase of understanding the client’s requirements, continued and frequent communications to align expectations, trasnparency around every step of the way and working together is what enables us to deliver quickly and efficiently for our clients.

3. Frequency of major platform updates

Upgrading once a year means users can plan ahead for major platform upgrades, request training for new functionalities, and the upgrades are free.

Each upgrade is communicated in advance through a client release detailing new functionalities and, if they are interested in any of the new functionilites, users can schedule the time

they suit them best for a training session. The client is the pilot for the upgrades.

4. Level of functionality coverage

There is a variance amongst the functional coverage but again with titantreasury this is driven by the client and their constraints. We believe in giving options to the clients to ensure the solution matches their needs, overcome their constraints and deliver on their objectives.

Beyond that we believe that there is a 5th reason why titantreasury stands out from the best TMS vendors available.

The 5th is the most important reason in our view. In the words of Deloitte’s own experts:

“Companies should make vendor and technology decisions that ‘best fit’ their individual businesses. This includes a vendor that understands your requirements, has the right deployment model, can integrate best resources of both teams and provides an application where the ‘feel and fit’ is in tune with the existing application landscape.”

5. Understanding the client and working as an extension of their team

At Centrus we believe in putting people first. That means understanding the client and working together every step of the way are essential part of how we work.

Although this is a key criteria when chosing the best TMS solution, it is a very difficult one to measure with a technical survey and RFPs like what has been done historically. However, for Centrus this is a key part of the project delivery, and our team works closely with clients, asking for feedback and quickly implementing the necessary actions to get to the best outcome possible.

titantreasury empowers treasury professionals to focus on value.

We help clients such as Pennon Group, Orbit Group, Irwell Valley Homes, A2Dominion, Carrefour, Accor Hotels and many others to make their lives easier.

If you’d like to like to book a demonstration with our team, please contact Gilles Bonlong, Director – Centrus

In speaking of social housing borrowers looking at overseas investors, if considering institutional investor funding, international markets should be taken into consideration by larger borrowers with the relevant treasury resources to manage more complex processes, on-going monitoring, and appropriate risk management. Accessing new investors engenders increased competition and access to wider capital pools for borrowers.

Due to increased sector awareness abroad stemming from investor education on the sector we’ve seen an increasing number of transactions involving non-UK investors. Unsurprisingly, large pools of capital potentially interested in Social Housing are based in other developed financial markets such as US, Europe, Nordics, Japan, Hong Kong, and Korea. Each of these markets has its own specific characteristics and preferred formats in which institutions (largely insurance companies, pension funds and asset managers) prefer to invest.

Attractions of the US market

The largest international capital market is the US; this private market is well established and deep dating back to the 1990s. The US private placement market is also the largest alternative funding market for UK Housing Associations. Over the last couple of years HA borrowings from the USPP market amounted to over a couple of billion £this continues to grow. US Investors are attracted by regulation, stability, the strong ratings of Housing Associations, and to a lesser extent the secured nature of obligations. With the USPP markets scale, low exposure to the UK HA sector, and capacity it provides a good alternative to the domestic UK market where some native institutions have very high exposures; M&G alone have almost £5bn of housing association debt across public and private paper. Sanctuary was one of the first HAs to issue an USPP and has borrowed over $400m from US investors with the most recent unsecured issue in March last year.

Other UK housing associations accessing the USPP market in recent years include Vivid, Newlon, Network Homes, Octavia, Stonewater and Bromford. Large borrowers such as Peabody, Circle (now Clarion), Orbit, and Places for People have also previously accessed the US market.

The main attractions of the USPP market are a large investor base along with interest in the sector, competitive pricing, large ticket sizes, and options for bilateral or “club” deals. The UK market has primarily evolved around just bilateral deals. USPP documentation is similar to a UK Note Purchase Agreement (“NPA”) apart from US representations and cross currency swap break language which is required by most US investors. Issuers receive GBP funding and most investors execute the swap on their side but require a swap break cost indemnity in the event of optional prepayment by the borrower. Borrowers may choose to fund in USD and swap the currency themselves. However, in most cases, UK borrowers across different sectors will prefer the US investors to hold the swap. Covenants tend to include asset cover with interest cover and sometimes a gearing covenant. The exact suite will depend upon the credit quality and size of the borrower. US investors are willing to provide unsecured funding as well and more amenable to this format than their institutional counterparts in the UK. We have seen some borrowers accessing the market with secured and unsecured tranches and the premium for unsecured tends to range between 30-50bps depending upon market conditions and credit quality. The USPP market tends to prefer medium-dated maturities ranging from 15 to 25 years with a maximum term of 35 years.

From a relative value perspective, the competitiveness of US investors depends on spread levels for similarly rated domestic issuers in the US, general credit perception, appetite, and the cross-currency basis swap. The impact of cross currency basis has deteriorated since early 2018 due to movements in the GBP/USD exchange rate, however we still see UK issuers entering the US market as credit perception and general appetite still provides scope for investors to provide tight spreads.

Asia and Europe

Beyond the US market there has been interest in the UK housing sector from other region driven mainly by the highly rated nature of the sector (for Asia) and the Environment, Social and Governance (“ESG”) investment angle (for Europe and Nordics). These markets have a less established track record but we are seeing rising appetite from investors based in Korea, Japan, Hong Kong, Europe and Norway. Korean insurers provide GBP funding and, in most cases don’t require swap break cost language. Preferred documentation tends to be as listed MTN but loan/PP formats can also be used. Less value is assigned to security as Asian investors value a wider spread over security. We’ve seen pricing competitive or in line with UK markets at ticket sizes of c. £100-150m per name from Korean investors. Japanese investors are less active and require the issuer to do the swap. They can, however, be very competitive for unsecured funding provided the issuer does the swap (Notting Hill and Places for People have accessed the Japanese market in the past in smaller sizes of c.£50m per transaction). Asian investors provide shorter tenors; up to 20 years for Korea and 12-15 for Japan. Lastly, the Hong Kong market is similar to the Japanese in terms of demand and number of transactions.

We are seeing some investor demand from Europe (mainly Germany and Benelux) and Norway. Unlike the US, European investors typically don’t do cross currency swaps themselves and require issuers to swap. There have not been many transactions in Euros with Places for People accessing the Euro market to date, however we expect issuance in Euros to pick up as we see increased interest from investors in the sector driven by ESG targets.

With the UK housing association market becoming a more internationally recognised asset class and borrowers increasingly sophisticated in accessing these markets, we expect activity with international investors to grow, providing healthy competition for domestic institutions.

IFRS 9 was tagged as the accounting standard that would remove complexity around the accounting for risk management strategies.

One year on from the mandatory adoption date we review how some of the key headlines of the new standard have been received and how it has impacted the risk management activities of corporates.

The unprecedented volatility in financial markets that has been witnessed in recent times has brought increased scrutiny from investors on how companies are managing risks and shareholder wealth. Those that have decided not to hedge certain market risks in recent years have been impacted by this volatility as a) the market negotiated its way through both the highs and lows of Brexit and b) for some companies, the increase in oil prices from $40 per barrel to $65-$70 per barrel.

Figure 1: GBP-EUR spot exchange rate

Those entities that have actively sought to manage these volatilities have performed stronger over the same period by fixing prices by using derivatives.

Figure 2: Brent Crude Spot Price

Where an entity has navigated this difficult time through effective risk management, the good work can often be eroded by not obtaining the right accounting result for the instruments used as part of these strategies.

IFRS 9 was intended to address this through aligning an entities risk management strategy and objectives with the accounting for this strategy by making the application of hedge accounting for financial instruments used in economic hedging activities more achievable. One year on we take a deeper look at how the introduction of IFRS 9 has made some hedge accounting strategies better or in some cases worse when it comes to the accounting.

Although the 80-125% rule has been abandoned under IFRS 9, the need for the calculations to assess this still exists.

Hedging Risk Management Components and IFRS 9 (Commodities, Interest Rates and Inflation)

The new rules introduced under IFRS 9 were aimed at ensuring entities could, if they chose to, manage their risk exposure in the most efficient manner available. The intention of allowing corporates to identify the individual risk components within both financial and non-financial host contracts was to ensure that if there was a derivative that could be acquired to match the dominant variable component within these contracts then the accounting should follow this matched relationship and strategy.

As a result, entities across infrastructure, utilities, retail and various other corporate sectors have undertaken widescale reviews of their existing commodity and interest rate risk management strategies in order to identify the dominant components they are exposed to variability in.

For companies exposed to commodity risks IFRS 9 has resulted in easier application of the hedge accounting requirements with many entities now able to achieve critical terms matching with their hedge strategies as a result of aligning the terms of instruments traded with the exact terms of the contract they are exposed to. This has been the achieved through in-depth analysis of contracts to identify the exact variable pricing and ensuring that the traded instruments align in order to remove the possibility of ineffectiveness in the strategy and ultimately the accounting at the outset.

Inflation – Hedge accounting solutions for inflation linked derivatives as a component of nominal interest rates exist and have been implemented. However, this has become an area where the rules around a component being separately identifiable and measurable have meant that this can only be achieved in certain circumstances.

Companies that have not yet done so should be undertaking a comprehensive review of existing customer and supplier arrangements to ensure that there is no margin erosion as a result of unidentified components that could have been hedged and subsequently hedge accounted for.

80-125% Testing (Operational Application of Hedge Accounting)

This was the headline act of the IFRS 9 hedge accounting module for many corporates. Immediately this was seen as a way of making hedge accounting operationally easier and would result in less cost associated with systems, controls and auditor overruns ensuring that the 80-125% testing requirement of IAS 39 was met. In practice, one year on and as a result of conversations with auditors companies are beginning to realise the measurement of ineffectiveness in economic relationships is still required and although the 80-125% rule has been abandoned under IFRS 9, the need for the calculations to assess this still exists in order to be able to accurately measure the ongoing journals required to apply hedge accounting.

Those hedge accounting relationships that contain mis-matches between the instrument traded and the item it is intended to hedge will always require quantitative assessment in order to measure the extent of the offset between item and instrument and allow a company to accurately reflect this in their accounts.

While the economic relationship assessment can often be a qualitative exercise in line with what was outlined in the designation documentation for the hedge accounting relationship, this only determines whether an entity can apply the concepts of hedge accounting under IFRS 9.

The dollar offset method that many companies used to assess the 80-125% test in the past now acts as a measure of how much hedge accounting a company qualifies to apply under IFRS 9.

Ultimately what companies have found is that auditors would like to see both the assessment of an economic relationship on a prospective basis and the measurement of ineffectiveness on a retrospective basis for a company to meet the requirements to continue to apply hedge accounting to their economic risk management activities under IFRS 9.

Companies should consider their current risk management activities and hedge accounting being applied to determine whether they may need to keep hold of the systems and processes they had under IAS 39 and re-purpose them to meet the requirements of IFRS 9.

Costs of Hedging (Options and FX Risk Management)

In response to concerns over accounting for time value on option contracts and for currency basis within fair value hedge relationships both resulting in profit and loss volatility under IAS 39, the IASB introduced a new accounting treatment for these unavoidable costs associated with carrying out a hedge strategy. The new rules allow for the deferral in a separate cost of hedging reserve within equity for these costs of hedging, therefore benefitting those entities that use options to hedge and have fair value hedges impacted by cross currency basis.

However, by addressing the accounting for currency basis as a specific item within the standard, this has resulted in less complex hedging strategies being impacted by the requirement to deal with currency basis as a cost of a hedge relationship.

For example, many corporates exposed to FX risk have in the past employed simple strategies of using FX forward or swap contracts to manage this risk. In hedge accounting for these the assessment of an economic relationship (or hedge effectiveness under IAS 39) was often a qualitative exercise without the need for any complexity in the valuation.

As a result of the costs of hedging rules being applied to currency basis and with currency basis being priced into FX forward and swap contracts, corporates are now having to perform a complex valuation exercise in order to identify the value attributable to currency basis where they continue with their existing strategy of designating forward rate risk as the hedged risk.

In many cases this turns out to be an immaterial amount for the purposes of the financial statements but is still required to be calculated adding a layer of complexity to what was a less than complex hedging strategy that did not exist under IAS 39.

This has been a key focus area for auditors in the first year of IFRS 9 application as many companies that have used instruments such as cross currency swaps get to grips with explaining currency basis to investors within the accounts and why the balance of this within their overall derivative MTM has moved materially over the last number of years. Companies that have considered using options as part of their hedging strategies in the past and avoided due to the complexity in the accounting should dust off these plans and review whether they are now fit for purpose in combination with the easier application of hedge accounting.

Those companies using instruments such as cross currency swaps should ensure that at the outset of any hedging strategy, they fully understand the components of the pricing and how these may impact the accounts over time. This aspect of IFRS 9 has the potential to be operationally complex in the future if not set up correctly at the beginning.

Key considerations for Corporates and how Centrus can help with your risk management strategy:

• Review current risk management policies to determine if they are fit for purpose; • Cost vs. Benefit analysis around hedging of identified risks; • Review current hedge accounting processes for IFRS 9 impacts and quantify; • Ensure required data is available to perform relevant assessments required on an ongoing basis; and • Benchmarking risk management practices against peers.

Corporates should ensure that they are undertaking a review of their current risk management landscape and ensure they are doing enough to protect their company values through these times of uncertainty.

Conclusion

While companies are still navigating their way through the finer points of the IFRS 9 implementation process arising as part of the first year-end under the new standard, the final impacts on hedging activities and whether the adoption of IFRS 9 has revolutionised the way Corporates manage risk remains to be seen.

A key point to understand in relation to hedging is that if you have an exposure to risk (commodity price, interest rate, foreign exchange , inflation or otherwise), doing nothing about the risk is in effect doing something – it is deciding to take the risk and allow your performance to be impacted by its variability.

In this article we look specifically at commodity risk and a basic vanilla hedging strategy.

What is Commodity risk?

Commodity risk is the financial uncertainty caused by fluctuations in the price of commodities. These fluctuations are beyond control and affect future market values and future cashflows.Commodity prices can be quite volatile partially because of their supply-demand dynamics. In addition, geo-political risk is another important inflence factor.

An important starting point in the process is to identify the commodity risks that a particular company is exposed to. Once identified, make sure you understand how these risks impact future cash flows.There can also be a significant impact due to foreign exchange rate movements. This depends on the currency that your company functions with.

For example, if you company operates in Euros and you do not hedge your fuel costs, the company will be exposed to EUR/USD movements over the period. These can be underlying benchmark price movement (likely Dollar denominated). Some large shipping companies saw their fuel costs increase by 13% in 2017 becasue of fuel costs/bunker price increases.

The table below illustrates the impact on commodity price movements to revenue and profitability:

Commodity price movements

Why Hedge the Risk?

Implementing an appropriate commodity hedging strategy can help provide more budget certainty, help manage liquidity and result in a smoother cost profile and limit operational risks. An appropriate commodity hedging strategy implementation can help you limit financial risks. Having a strategy in place helps to:

provide more budget certainty

to manage liquidity and as a result

to achieve a smoother cost profile

Again, not hedging when you have an known risk is a decision in itself. You sould not underestimate the potential impact of overlooking the risks.

How can I hedge the risk?

It is essential to have a robust approach to your hedging strategy. This means achieving the right level of oversight and the relevant approval procedure. The below outlines the high-level approach to implementing a suitable hedging strategy:

High-level hedging strategy

Consumers use fixed-rate swaps to hedge their price risk by fixing or locking in their fuel costs. This happens accross many indutries such as air, marine, rail and road transport. Sellers of commodities also use fixed-rate swap strategies for inventories as well as price risk management.

To illustrate how a hedging strategy can work from a consumer perspective, let’s take the example of a shipping company. This shipping company wishes to hedge 75% of its bunker consumption over the coming year. Say the company consumes 120,000 Metric Tonnes (MT) of fuel oil and they would like to hedge their price risk on 90,000 MTs over a 12-month period (from Jan 18 to Dec 18) – allocated evenly.

The shipping company can do this by entering into a fixed-rate swap on the benchmark (e.g. 3.5% Fuel Oil Rotterdam) for 7,500 MT per month at e.g. €305 per MT.

Let’s have a look at how that would play out for the shipping company over a 12-month period:

Fixed Rate Hedging Strategy (Example)

Example of fuel price & costs under the different scenarios in 2018

As you can see from the table and graph, if the shipping company had passively accepted the price risk over the 12-month period, they would have had significantly higher (€2.7m) and less predictable costs.

Therefore, using a simple fixed-rate swap strategy, the shipping company in this example has reduced total fuel costs, proactively managed their price risk and stabilised their ability to forecast costs. However, it is important to note that if the price had moved the opposite direction over the period, there would have been a missed opportunity for cost saving on the hedged part of fuel costs. This is the cost of implementing an effective hedging strategy which mitigates price risk and stabilises the cost line.

Moreover, from an accounting perspective, it will be important to be in a position to put hedge accounting in place on the trades to reduce any Mark-to-Market volatility on the P&L.

In the following articles we will explore a variety of hedging strategies depending on risk appetite and business requirements.

If you would like to discuss your hedging needs across any asset class (Interest Rate, Commodity, Foreign Exchange, Inflation etc.) do not hesitate to get in touch with us.

Centrus provide independent advice on hedging strategies and support through every stage of the process. From assessing risk and developing an appropriate hedging strategy through to execution and accounting impact post implementation.

Given the consolidation in the housing association sector in recent years, we often point out that the largest HAs are bigger than their FTSE 100 property equivalents on most measures. The next tier of HAs below that are also now very large corporate entities. One consequence of this is that we are seeing a steady move towards a re-setting of the relationship between these borrowers and their banking groups in the context of a clear strategy.

As legacy bank liabilities steadily amortise, are restructured through mergers, or are replaced with more sustainable market level funding, banking portfolios are looking more like those of other property-owning businesses. HAs have more willingness to restructure their banking relationships and address legacy lenders’ concerns when the result is tailored to support the needs of the HA as borrower. As legacy issues reduce and new lenders come into play, banks are better placed to provide responsive and flexible support through balance sheet, underwriting and ancillary services and take their rightful role as “enablers”.

One good example of this progress and shift in relationships is the increasing provision of “bridge to bond” facilities from HA relationship banks.

Bridging Loans in an HA Context

For HAs, bridging facilities typically provide committed liquidity until they can issue into the public bond markets. As well as providing greater flexibility, bridging facilities also provide an opportunity for HAs to expand the relationship with their key lenders.

In this context, bridging loans are often very short term (2-3 years) with the potential for some or all of that period being unsecured. Mandatory repayment clauses force prepayment and cancellation upon DCM issuance and fee structures incentivise refinancing – the facilities are really meant to be bridges after all rather than “emergency liquidity”. In other sectors the term can be shorter still but given the vagaries of property investment timetables we see it as worthwhile HAs pushing for the longer end of this range.

Key benefits of Bridging Loans

Efficient Liquidity Provision – a period of being unsecured means that committed liquidity can be provided at short notice and low cost, with underwriting often sitting separately from core relationship lending teams.

Mitigate Execution Risk – the provision of committed liquidity affords some flexibility to the issuer and allows them to enter the market on their own terms rather than being a forced issuer.

Leveraging Existing Bank Relationships – by involving a borrower’s core relationship banks, concessions can be gained in legacy facilities as part of the overall relationship package.

Centrus’ Recent Experience

We have recently seen a number of bridges taken by HAs for a variety of reasons and with some interesting nuances in the structures.

One client focussed on the bridge mainly as a vehicle for mitigating execution risk: the purpose of the bond was to refinance existing facilities and the security to be released was required as collateral for the new bond. By arranging the bridge it allowed the issuer to prepay an existing lender, release the security and subsequently allocate as collateral to the bond in a timely manner without risking execution.

A simultaneous bond issuance, prepayment and security release is of course possible, but removing complexity from the primary issuance (alongside the flexibility to issue to the issuer’s own timeline) was seen as a prudent approach that reduced risk in the context of an already complex set of transactions.

Interestingly, this bridge was also dual-tranched with the second tranche coming online once the first bond had been issued: this provided further flexibility for the issuer whilst retaining an efficient fee structure. The RFP process also involved a request for concessions on existing facilities, reinforcing the idea that mature banking relationships should be mutually beneficial – the stick and the carrot both have their places!

Another recent example which undoubtedly highlighted banks’ ability to be responsive and supportive occurred towards the end of 2018: a three week process – from RFP to execution – focussed minds and led to an excellent result for the borrower.

With three banks on board to split the substantial bridge requirement the decision had to be made between a syndicated facility or bilateral agreements. Syndicated bank facilities are more of a norm with large corporates and utilities and, in our view, a move to more mature banking relationships in the HA sector might in part involve a renewed appetite for large syndicated liquidity facilities. Some of the banks had a preference for a syndicated approach where they felt they would have more visibility of the overall transaction, given the low pricing of the bridge funding.

A syndicated facility simplifies documentation, but the entire process could be held hostage by the slowest moving bank. A series of bilateral facilities, on the other hand, would require three separate agreements to be negotiated and documented within the three-week timeframe but would allow execution of just part of the requirement if, for example, only two of the three agreements were finalised.

In this case the decision was made to pursue three bilateral agreements and it paid off: two agreements were swiftly executed with the third also finalised within a very narrow timeframe. Good relationships and open communication helped considerably.

Bridging the divide

Our view is that building better managed relationships with top tier banks via additional ancillary business (DCM, acquisition finance, liquidity facilities, hedging etc.) is a win-win: the banks like the deeper relationships and the erosion of legacy portfolio value naturally makes them more enthusiastic. The quid pro quo is that for HAs with ambitious development programmes, legacy debt has sometimes been a block to progress.

This article has focussed on bridging loans, which give flexibility for HAs looking to enter the public bond market (or indeed other capital markets). On one level they are simply another example of how banks’ direct balance sheet support is now focussed on the short term, but if used effectively they enable borrowers to align funding with the needs of the business. Bridges need to be tailored rather than “taken off the shelf”, but they can help to manage risks around funding investment programmes and thus be a good example of using banking relationships to support the wider business.

For more information, please contact Lawrence Gill, Director – Centrus

Responses to the initial call for evidence for the Williams Rail Review are being submitted and the rail industry is awaiting the findings which are due to be published in Autumn 2019. The Rail Review is far-reaching and makes for a complex task for independent chair, Keith Williams, and his team if they are going to make recommendations for meaningful change.

As the industry awaits its conclusions, this paper considers a question that has been posed multiple times yet remains pertinent to all the principles set out in the Rail Review’s terms of reference:

Can there be a role for private finance in the delivery of UK rail infrastructure and, if so, how can a pipeline of opportunity be created?

As we move further into 2019, one of the big picture trends we are seeing in the UK social housing sector is a real diversification of funding strategies and sources. Pre-2008, with one or two exceptions, banks had a near monopoly on lending to housing associations via long term facilities and embedded or stand-alone swaps. The period between the global financial crisis and 2018 (again with notable exceptions in US and other currency PPs and a handful of retail bonds) saw the banks retrench to mainly 5-year funding and the UK institutional market (in the shape of public bonds and private placements) dominating the market for long dated funding, almost entirely in secured, fixed rate format.

As sector business models and strategies continue to diversify, we are perhaps starting to see a break down of the old “one size fits all” funding mechanisms and the development of a much wider range of funding solutions and sources for HAs which are more bespoke to the needs of the business. Examples include;

Increased use of unsecured bridging facilities from banks in order to secure liquidity and reduce timing/execution risk of capital markets issuance in potentially volatile markets

Issuance of Floating Rate Notes rather than the usual fixed rate format as many borrowers have become over fixed in recent years

Use of local authority lending for development, revolving and longer-term facilities

Increased use of unsecured funding from both UK and non-UK investors in order to increase flexibility and as loan security becomes a constraint within certain organisations

More direct funding into joint ventures and non-recourse commercial entities within groups in order to reduce reliance on on-lending or investment from the regulated entity

Greater willingness to access non-UK investor markets in order to retain pricing leverage and arbitrage pricing basis between GBP and other funding markets (e.g. US, Euro, Korea)

New group funding vehicles such as THFC’s bLEND and MORhomes

There has been a fairly consistent narrative in recent years that housing associations are getting a “raw deal” from sterling investors. When you look at pricing levels for sometimes weaker rated utility companies, for example, it is difficult to argue against this. Nonetheless, we would argue that the housing sector has perhaps played into the hands of UK investors by effectively signalling to them that they are the lender of first and last resort. This is in marked contrast to many issuers in the utilities sector, which play off sterling investors against the USPP and other non-GBP markets in order to tightly manage their funding costs.

This is borne out by some recent examples such as National Grid Electricity Transmission (A3/A-/A) which recently issued its first new sterling bond transaction since 2012 (excluding the liability management exercises undertaken as part of the Cadent de-merger in 2016) and only the second in the last 10yrs. The 16-year deal priced at G+120bps, significantly tighter than recent similarly rated housing deals. More recently, Bromford issued 20-year USPP the pricing of which we understand compared favorably both to its own secondary sterling bonds and recent issues by large HAs in the sterling market.

We see the challenge to established market orthodoxies as a healthy development for the social housing sector. As ever, changes to tried and tested funding mechanisms need to be fully understood from a risk management perspective and boards need to be comfortable with any associated treasury risks. For example, improving pricing dynamics by accessing a non-UK investor base may (where investors do not have natural sterling appetite) bring with it a degree of FX risk – whether contingent on pre-payment or outright, where the borrower swaps back into GBP. While these risks are manageable, they do need to be properly understood and capable of being monitored and managed from an operational perspective. This may preclude smaller organisations with less sophisticated and lower resourced treasuries which may opt for more vanilla funding structures.

MORhomes was of course predicated on its ability to address a number of sector challenges around pricing, ease of market access and structure. It is fair to say that we were always somewhat sceptical as to whether it could deliver on its stated objectives around pricing (other perhaps than for the very weakest credits) but had no evidential basis to support this. However, the spread on its debut issue of 190bps now provides a clear benchmark for HA borrowers weighing up their options, including own name approaches and the more competitively priced THFC aggregation vehicles. It is certainly clear given what we are seeing in the market that for larger and/or stronger credits, MORhomes (taking assumed additional enhancement/vehicle costs into account) is probably somewhere in the region of 40-60bps more expensive than what these borrowers might achieve in their own right. Even at the smaller/weaker end of the credit spectrum, it is likely that many borrowers would be able to achieve comparable or better pricing in their own name, although some may see non-pricing benefits in terms of structure and/or speed of execution (at least in respect of future transactions).

More generally, we fully expect this divergence trend to continue, bringing with it significant benefits for housing associations seeking both to minimise their cost of funding and to tailor debt structures to the specific needs of their businesses.

Bill Cumberlidge, Managing Director of Centrus Aviation Capital was invited to take part in a panel debate during the Airline Economics Growth Frontiers Conference in Dublin this January.

The panel gathered over 1,800 people to discuss “New and Midlife Aircraft market dynamics”.

Some of the questions were:

With new aircraft production problems causing delays, what is the knock on effect on the midlife aircraft market (values and extensions)?

What do you think about the extension of leases during the latest industry events?

What is your view on airline bankruptcies and the effect it has on lessors?

If you are interested in investing in Aviation, please visit www.centrusaviation.com

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you agree to our Privacy Policy

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.