Centrus Analytics is the technology branch of Centrus. We help organisations improve efficiencies and control with technology-led solutions, including:

Hedge Accounting and Valuations : supporting clients with hedge accounting requirements including strategy, effectiveness testing and documentation. Our platform is also built to perform complex valuations on vanilla and complex financial instruments.

Treasury Management System: titanTreasury is designed to support treasury functions and flexible business operations, giving your team greater visibility and control.

Data: Our data solutions unlock insight into opportunities that our clients can take advantage of by transforming data into information, and that information into actionable knowledge.

For more information, or to book a demo, please contact Gilles Bonlong, Head of System Implementation

Heightened market volatility, a sharp rise in global interest rates and increased flexibility for restructuring derivatives has reignited queries from our clients about derivative valuations and restructuring or unwind costs. Large swings in the value of derivative portfolios have put ever more scrutiny on accounting valuations and how these are presented in accounts.

In this refresh of the original 2017 white paper, we take a refreshed look at derivative valuations:

1. Mark-to-Market of a derivative or ‘mid MtM’, represents the Net Present Value of all future projected cashflows to be received and paid, discounted at a risk-free rate (SONIA, SOFR, €STR). This is valued on the same basis as that typically received in valuation reports from banks and is still often used for accounting purposes.

2. Transaction value of a derivative is the ‘Mark-to-Market’ taking into account credit, bank funding, regulatory capital implications as well as trading costs. It may also factor in the bank’s (or corporate’s) wider derivative portfolio, wider strategy, and commercial considerations. These factors may impact a derivative valuation when unwinding or restructuring a derivative prior to maturity.

3. Accounting value of a derivative can be the same as the ‘Mark-to-Market’ described previously, but increasingly often takes into account certain accounting valuation adjustments that depend on the relevant accounting standard. 10 years on from its implementation, IFRS13 puts a greater emphasis on credit valuation adjustments to the ‘Mark-to-Market’ for accounting purposes which mirror a transaction value. In some cases a funding valuation adjustment is required too.

I made my inaugural visit to the All Energy and Decarbonise conference in Glasgow SEC last week with members of our Infrastructure and Energy Transition team , whose positive feedback on the event was unanimous: it was a productive, dynamic occasion, well attended by key players in the energy transition network.

Below is a snapshot of what I found to be the most compelling messages cutting through.

Less mouth more trousers

Globally we have bold 2030 investment and 2050 net zero commitments in place, but as the clock ticks and the breaching of our planetary boundaries becomes increasingly terrifying; the time for talk has passed and we need action and delivery.

In Glasgow, it was reassuring to see the huge range of technology and project development that is already on the table. Exhibitors showed off pioneering assets across wind, solar, hydrogen, marine, private wire, hydro, interconnection, carbon sequestration and energy storage. With consumer expectations adding huge weight to the support they need, we are seeing decisions on execution and investors becoming bolder with the risks they are taking. Private and Public Sector funds are now going where the problems are.

Swap the plans and promises with action

The presenter’s lineup was strong. In the opening plenary session, Jacqueline McLaren, The Lord Provost of Glasgow, Humza Yousaf, First Minister of Scotland, David Bunch, Country Chair of Shell, Chris Stark, CEO of the Climate Change Committee and Susan Aitken the Leader of Glasgow City Council took to the stand. They shared their concerns and conflicts, but they also shared their commitment, raising their hands to admit that disagreements need to be put aside. Together they recognised that scientific, public, corporate, council and government teams need to collaborate on the common net zero targets if we have any chance. This hope was backed up by the exhibitor population from across all pieces of the puzzle. The development across the renewable energy product life cycle is gathering pace every week and it was underpinned by a common theme of less talk and more action.

‘Just’ must be everywhere

The other message that resonated for me was the recognition that the word ‘just’ has to play a key part in every component of energy transition. We must show that we have learned lessons from damage done by industrial change in the past – all close to home in Glasgow. We must include the education, social and people impact at every step of the way. Recognising the jobs and education opportunities that the green economy must grow was shouted about by the strong academic research in the visitor population as well as the carbon literacy and renewable energy studies from the students in attendance. It was impressive stuff.

Centrus exhibited in a central hot spot for attendee footfall: we were neighboured by Tesla, The University of Edinburgh, Shell and ETZ. The contributions from our energy transition and infrastructure corporate advisory team were very strong, with everyone working hard to show off the Centrus brand, our sector expertise and our credentials. We connected with over 100 new and existing contacts and will reach out to identify opportunities where we can provide support. B Corp as a certification was relatively unknown to this audience, (with the exception of Thrive Renewables PLC) and our B Corp branding raised many interesting discussions about the value of using your business as a force for good.

There was lots of promise: I hope that the pioneering ambition of Scotland’s renewable energy transition that was shown off at All Energy Glasgow 2023 translates into further operational examples by this time next year.

If you want to discuss the event, the themes arising or the role that Centrus is playing, please get in touch with George Roffey, Sustainability Officer – Centrus.

Another month, another bank rescue. Sounding like the beginning of a Star Wars film, the First Republic has been rescued! Or has it fallen? Banking stress in the U.S. and Europe is a reminder of how quickly confidence can erode. The rapid response by authorities was reassuring but the impact on the financial system of rising interest rates and falling asset prices is still playing out, with the US regional banking market the current focus. Are we in a credit crunch?

Long term gilt prices have been relatively stable in recent months. Looking forward the UK Government will supply plenty, with £240 billion of issuance per year until 2028 expected. With the Bank of England no longer a buyer, will prices fall and yields rise further? Asset reallocation is to be expected in a higher interest rate environment. And the pension risk transfer market is predicted to be red hot for the rest of 2023. That means companies looking to lock in their defined benefit pension scheme liabilities with insurance companies who in turn look to buy appropriate assets to offset the liabilities. There is still £1.5 trillion of DB pension scheme promises on UK corporate balance sheets. So, some support for gilts is to be expected, and one silver cloud for the sector is the demand for direct investment in social housing, infrastructure, and regeneration projects. Whether the extra supply of gilts will be soaked up and the Government (and everyone else) can avoid higher borrowing costs is the question.

Spreads on housing association bonds for A+ and A rated credit are broadly where they were a year ago having fallen and stabilised since the autumn volatility. Markets are favouring stronger credit and A- credit spreads are notably higher than a year ago.

Pressure on the social housing sector and its response

The Regulator of Social Housing reminded us of the pressure the sector is experiencing in its latest quarterly survey report. The average 12-month interest cover (excluding all sales) over the last three years has been 131%. For the year to December 2022, it was 102%, the lowest ever recorded and for the year to December 2023 it is forecast to reduce to 93%. The December 2023 outcome is driven by increases in projected spend on capitalised repairs and maintenance (£0.9 billion) and interest payable (£0.4 billion), offset by increased net cashflows from operating activities (£1.0 billion). If it were not for the 7% rent increase and the sector showing agility to control operating cost, it could be a lot worse.

The Regulator confirmed that several housing associations have obtained loan covenant waivers in response to increasing investment in existing stock, with 26 reporting having agreed a waiver to exclude the exceptional costs of building safety works from loan covenant calculations, and 22 waivers being reported in respect of energy efficiency or decarbonisation works. In our own development appraisal assumption survey, we noted that most respondents now have decarbonisation beyond EPC of C in their base business plans.

Based on our recent activity with clients, the housing sector is currently focused on redefining strategy and bank restructuring rather than raising debt in the capital markets. Appetite from banks is steady with key lenders still committed to growing loan books. There is a clear sense of impactful strategic thinking by the sector, and preparation for the future.

What next?

Further banking stress, inflation not falling or the economy not performing as expected are examples of what can weaken the outlook. Some investments will be difficult to justify in the higher interest rate environment and there is evidence of weaker liquidity in M4 money supply. But so far it would appear this era will be remembered for the impact on the financial system and the economy of high inflation and interest rates.

Whether we call this a re-set, a credit crunch or anything else doesn’t really matter. What matters is cautious and strategic financial management. The importance of strong liquidity and prompt re-financing is as important as ever. With the possibility of further contagion, counterparty risk is a critical consideration requiring careful allocation of investment assets.

For more information on any of the topics mentioned, please contact a member of our team or email london@centrusadvisors.com

A few years ago, we did some work around our brand and messaging with the excellent David Butcher of Communications and Content, the outcome of which was the adoption of a Centrus strapline that we’ve used ever since, Finance with Purpose.

One of the reasons I love Finance with Purpose as a core mission statement for our business is that it encapsulates three core aspects of what Centrus believes in:

1. Our People

Our people are our most valued asset and I’m incredibly lucky to be surrounded by such a great team. They bring high levels of energy, talent and engagement to their work, consistently delivering innovative solutions and successful outcomes to our clients. We are absolutely committed to making Centrus a great place for people to learn, thrive and enjoy successful careers, allowing our people to work with a real sense of purpose and commitment.

2. Our Services

We are a financial group committed to sustainability, real assets and essential services. We are fortunate to have built a market leading position across sectors such as affordable housing, education, energy transition, water, infrastructure and transport – all of which deliver useful outcomes and positive impact to society. We are committed to responsible finance as a purposeful and positive force in enabling high quality infrastructure, services and employment while offering stable and reliable long term investment returns to those who need them.

3. Our Business

We have a real passion and belief in business and entrepreneurship as a force for good. As well as generating economic growth, great businesses provide employment, career opportunities and a positive impact on the communities within which they operate. We have had a long held commitment to these values and our recent certification as a B Corporation underlines this belief and sense of purpose in what we do.

So, next time you see us using #FinancewithPurpose, hopefully you will have a better insight as to precisely what we mean!

Another week, another round of interest rate increases. With the Federal Reserve having led the inflation fighting charge on the part of Western Central Banks, its 25bp increase to a 4.5-4.75% target range represents an easing off of the rate of increases. With the Bank of England following on with a 50bps increase, taking its policy rate to 4% – a 14 year high – and the ECB also hiking by 50bps to 2.5%, the squeeze on indebted households and borrowers (including governments) continues.

In the UK and the US, the housing market is already showing signs of stress, unsurprisingly in the US, where the benchmark 30-year mortgage rate has gone from sub 3% to as high as 7% before falling back to north of 6% this is having a negative impact on both new housing orders and house prices, although, the effects seem to vary regionally. In the UK, December house prices fell for the fifth month in a row, the longest decline since the market correction in 2008-09, with mortgage rates in December averaging 3.67%, the highest in a decade. Savills’ latest forecast shows UK house prices falling by an average of 10% during 2023 – when even the estate agents are this bearish, you know the housing market outlook is gloomy.

For the UK, the dark economic outlook continued with the IMF forecasting that the UK would be the only G7 economy to contract in 2023, citing high taxes, increased interest rates, high energy prices and a squeeze on government spending. The IMF forecasts will place further pressure on Jeremy Hunt from his own backbenches to shift back to a more growth-oriented strategy in the forthcoming budget.

Improved sentiment in public & private debt markets in early 2023

Despite the various storm clouds, there were some reasons to be cheerful as the new year commenced. As we know, 2022 was a pretty ferocious year regarding funding markets and volatility across inflation, rates and energy costs. The resulting melee caught many off-guard with the result that public debt and equity markets ground to a virtual standstill at times with volumes massively down on previous years. Although private markets picked up a certain amount of the slack, price discovery becomes increasingly challenging without visibility of reliable public market benchmarks. Being a fickle bunch, investors appear to have rediscovered their nerve over the Christmas break and January saw record levels of issuance in the Euro fixed income market. Although Sterling was less active, there is a clear return of appetite and liquidity as reflected in new issue premia for primary bond issues which are tight to negative, underlining a major shift in investor sentiment.

This is also reflected in buoyant private credit and banking markets at the current time as evidenced by deals that we have in the market for housing, infrastructure, energy and real estate clients. As a result, borrowers are dusting off investment and capex plans which were quietly deferred last year and showing a greater willingness to re-enter funding markets, particularly with all-in rates significantly lower than the levels reached during the UK market spasms of last September. To put this in context, the underlying 5, 10 and 30-year gilt/swap rates are circa 1.5-1.75% down from the highs of last year and credit spreads are 50-100bps lower depending upon the credit rating and sector in question.

Although I appear to have missed my invitation, colleagues from our Investor Coverage team had the tough task of departing the UK winter and heading to the US Private Placement Industry Forum in Miami. The positive early 2023 tone was also very much in evidence from the many US institutional investors they met over there with a strong appetite confirmed for strong credits across affordable housing, real estate (secured and unsecured in both cases) and infrastructure. 2022 underlined the need for borrowers to maintain flexibility and access to different sources of capital and given the depth of the US market, this remains an important option for many debt issuers.

Given the gyrations of 2022, we are seeing a renewed focus on risk management across our client base across rates, inflation and power/energy costs. Even though borrowing costs have fallen materially, along with wholesale gas and electricity prices, clients are keen to take risk off the table and to lock down certainty in their business plans wherever possible, even if on balance they expect markets to move further in their favour.

So, in spite of the challenging backdrop, debt markets have very positive sentiment and strong momentum into February, which we hope will set the tone for the rest of 2023.

For more information on any of the topics mentioned, please contact a member of our team or email london@centrusadvisors.com

We wave goodbye to 2022 perhaps with more of a sigh of relief than a tinge of sadness. For it has been a difficult year in which hopes of a “return to normality” after the disruption of the COVID lockdowns were dashed by a confluence of events which have rocked households, businesses, economies and countries to their foundations and demonstrated the fragility of systems which operate without hitch for long periods of settled and benign conditions but which can break apart rapidly under stress.

Variously, 2022 brought us:

War in Ukraine – arguably the first major strategic armed conflict in Europe since WW2. Aside from the obvious and terrible humanitarian toll being inflicted, the knock on effect in geopolitical and economic terms is still unfolding, but will likely be profound. The sanctions imposed by the US and its strategic partners in Europe have fractured the global energy supply system and perhaps signalled the beginning of the end for the dollar-based global monetary system.

Leverage & fragility – in the second half of 2022 the UK experienced a financial convulsion on the back of the Truss/Kwarteng mini-budget. Exploding gilt yields led to a spiralling liquidity crisis for UK pension funds employing LDI investment strategies (basically leveraging assets to drive higher returns in a low interest rate environment) and ultimately forcing the Bank of England to capitulate and re-start its gilts purchase programme temporarily. While many viewed this as a UK specific issue, it was one of a number of rivets popping in an over-leveraged system with rapidly rising bond yields and a rising dollar. Other tell-tale signs were a massive provision of dollar liquidity to the Swiss Central Bank from the Fed, most likely to aid a well-known Swiss bank and the Japanese Central Bank being forced to ditch its 25bps peg on 10 year Japanese Govt bonds in order to prop up the Yen –a supposed safe haven currency whose value had dropped precipitously against the USD.

Inflation at 40-year highs – the energy crisis and broader supply chain issues saw inflation rising to multi decade highs putting further strain on household, business and government finances with the cost of living feeding through to demands for wage increases and widespread industrial action by public sector workers.

Interest rates – with Western Central Banks having long argued that growing inflationary signals were “transitory” in nature, they were forced to throw in the towel in 2022 and to spend much of the year playing catch up by increasing policy rates at an unprecedented pace with bond yields following a similar trajectory. It has become increasingly clear that Central Banks face the unenviable challenge of having to act to control inflation (politically a high priority), whilst minimising the impact on growth with many economies already heading towards a recession. The end of a 40-year bull market in interest rates and the end of an era of easy money experienced since the global financial crisis is likely to have profound effects on asset prices which were driven up by a combination of lower equity return requirements and cheap and easy debt; further impacting consumers sense of a reduction in wealth.

Energy Crisis – UK and Europe (along with other net energy importers) saw dramatic spikes in energy costs, partly as a result of sanctioning one of its major suppliers of oil and natural gas but also in part as a result of poorly thought through energy policies going back many years, including lack of strategic energy security planning and over reliance on intermittent renewable energy without the necessary storage technology to cope with this. This has led to enormous pressure on households and an existential threat to energy intensive industries in the UK and EU. Governments with already high debt to GDP ratios were forced to step in with energy price cap mechanisms –putting further strain on public sector finances.

Each of these issues in isolation would be a serious and newsworthy event. The fact that they happened concurrently felt rather like living through one of those “perfect storm” scenarios that businesses use as an extreme but highly unlikely set of events designed to test a business plan to breaking point.

In the immortal words of D:Ream and New Labour, surely in 2023, Things Can Only Get Better? We certainly hope so. We found 2022 a tough year to do business and we know that many other businesses are far more exposed to the above issues than those of us working in professional services and finance. Rather like after COVID, we would though caution against any near-term expectations of a “return to normality”.

Sadly, there appear to be few signs of an end to the Russia-Ukraine conflict and with the major powers directly and indirectly involved seemingly entrenched, escalation at this stage seems a more likely eventuality than peace.

While the energy crisis will likely give a long-term boost to the UK and Europe in terms of energy security, supply, clean energy production and energy storage, for the time being, those countries and regions which are self-sufficient in energy resources will be far better placed to ride out the crisis than those reliant on imports. And with government finances being stretched further from an already highly leveraged position, financing of deficits in a world where the natural marginal buyers of government debt (think China, Russia, Middle East & Japan) may no longer have the same appetite for debt issued by Western nations, there may come a point where these countries face an unenviable choice of paying more to borrow, raising taxes or cutting their cloth to reduce deficits into slowing or recessionary conditions.

While many in the financial markets eagerly await the much vaunted “Fed pivot” – i.e. the point at which Chairman Jay Powell throws in the towel on interest rate increases and rides to the rescue of an ailing economy and stock market, he continues to surprise pundits with his clarity of purpose and clear determination to continue on his hawkish path until inflation is brought under control. Perhaps he will eventually pivot, but it may well only be once the Fed has seriously broken something or other be that Main Street, Wall Street or indeed set off a global financial crisis of some shape or form – that political pressure on the Fed might force a change of tack.

Our advice for 2023

So, our cheery advice for 2023 is to hope for the best but prepare for the worst and in doing so, we would recommend the following:

Ensure that your business plans factor in the possibility of sustained and/or higher interest rates, sticky inflation and continued volatility.

Leave higher than normal risk buffers in business plans and credit rating scenarios.

Factor in higher than normal execution risk for any major financing, merger, acquisition or sale process and allow much longer for transactions to complete.

Prepare well in advance and earlier than normal for funding processes and ensure you have fall back options in case of further bouts of market disruption as experienced in 2022 –strategic flexibility will remain key throughout 2023.

Consider the impact of higher cost of debt and equity capital on asset prices – although this hasn’t been clear across all asset classes, it is reasonable to expect an on-going adjustment as buyers and sellers adjust to a new normal.

Be aware of the higher propensity for political interventions as pressure increases on the government to assist under pressure households and businesses and control government finances.

Assume energy costs remain elevated for longer with associated impacts on EBITDA, and plan the energy strategy and narrative around outperforming those assumptions.

As ever, the team at Centrus is here to support our clients in navigating these choppy waters. If you would like to contact a member of our team or want more information on any of the topics mentioned, please email london@centrusadvisors.com

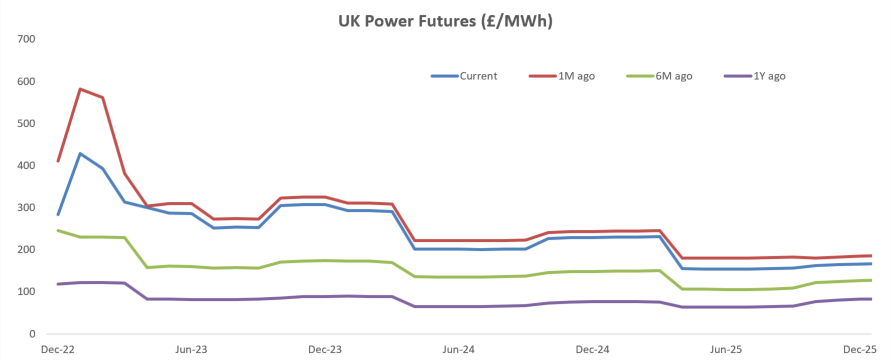

In December 2022, The UK Government is proposing to bring forward legislation for a new levy on UK electricity groups generating more than 100 Gigawatt-hours (GWh) per annum. The idea is to subject “Exceptional Generation Receipts” to a new 45 percent levy which importantly will not be deductible from profits subject to UK corporation tax. The levy will operate between January 2023 and March 2028.

The UK Treasury recently published their proposed calculation of the levy in their technical note. This calculation is as follows:

£m

Generation Receipts

XX

Less £75m* UK generation in Megawatt-hours (MWh)

(XX)

Less a Group threshold allowance

(10)

Receipts subject to Levy at 45%

XX

Source: UK Treasury Technical Note: “Electricity Generation Levy”

What is the problem?

As is common with hastily considered tax measures, the devil is always in the detail and there are usually unintended consequences. The consequences that we see in this instance are:

1. The Levy was sold in the press as a windfall tax. Unfortunately, it is not – it is a tax on a proportion of revenues not profits.

As a result, the measure risks taxing groups that have properly incurred costs which are subsequently not being offset in the calculation of the levy. By example, those generating electricity to offset usage within their groups need to create formal intercompany contracts rather than selling to the market as a hedge. Failure to do so risks incurring the levy with no offset on the market price paid by another part of the group. As prices rise, this lack of offset becomes punitive, particularly as the levy is not off settable for corporation tax.

2. The Levy risks distorting the market for renewable generating assets with the thresholds being introduced.

Whilst we think the allowances and generation volume thresholds are sensible to avoid bringing too many companies into the levy regime, there is a risk of market distortion as a result. The size, scope and post-tax nature of the levy, together with near term forward prices means that the levy will have a material valuation impact for some but not all current and prospective owners. Those groups with limited current generation will have a significant competitive advantage over the larger generator groups.

What is next?

The proposals are being drafted into law and will be available for view next month (December 2022) ahead of the levy being introduced in January 2023. Whilst we hope that some of the unintended consequences will be ironed out, we think it is unlikely that all of the issues will be addressed given the rushed timeframes.

If you have any questions please contact Geoff Knight, Managing Director – Centrus

As housing associations’ finances come under increasing pressure, how much will unsecured borrowing have a part to play? Gary Grigor of Devonshires and John Tattersall of Centrus Financial Advisors assess the situation

The housing sector has been hit by a number of challenges in recent months. What began as a cost inflation challenge quickly became a more acute operating margin challenge in the face of unspecified caps.

With borrowing costs now far higher than originally forecast, interest cover covenants are coming under increased pressure.

The pan-sector response is still in development, but capex is likely to slow in the short term and efficiency savings will be needed.

Liquidity requirements are likely to fall too, as the temptation to reduce facilities and save carry costs to optimise interest cover performance appeals.

This strategy has risks, though, particularly where it takes time to put new facilities in place should requirements pick up again.

It is in this context that unsecured borrowing may have a strategic part to play.

Unsecured borrowing allows registered providers (RPs) to dispense with providing and maintaining a ring-fenced pool of property security either via a security trust mechanism and/or direct charging to the relevant funder.

Instead, the organisation must maintain a pool of unencumbered assets for the life of the facility. The upside of this is that the time, effort and expense associated with pledging a ring-fenced pool of property security under conventional funding arrangements is dispensed with, paving the way for a quicker and more decisive funding solution.

Unsecured borrowing can also be scaled up and down far quicker than conventional secured funding.

While an unencumbered pool of assets must be preserved at all times, there are not the same rigorous due diligence requirements to be satisfied.

Provided that the unencumbered assets stack up to meet the minimum threshold from a valuation perspective, then that, in itself, will be sufficient.

As a result, the composition of the unencumbered property pool can also dynamically fluctuate over time, facilitating easier asset management and offering protection should asset values fall, as potentially forecast next year.

The Pros and Cons

Pros

Speed of execution: With no security charging process, facilities can be executed and available comparatively quickly. They can also be restructured and re-sized with greater ease. Unsecured facilities can offer strategic value where a debt capital markets programme is in train, but the timing is not quite right to launch.

Flexibility: Release and substitution mechanics do not apply, so managing the unencumbered asset pool is generally straightforward – helpful where stock rationalisation is under way.

Sweating the asset pool: Most portfolios have assets that wouldn’t otherwise be acceptable to a funder yet can still generate borrowing capacity via the unencumbered pool.

Cons

Cost of carry: Margins and fees tend to be higher for unsecured facilities, albeit the differential to secured facilities has meaningfully narrowed in recent years, particularly on an undrawn basis (as low as five to 10 basis points per annum in some cases).

Shorter tenor: To further offset the cost difference, most unsecured facilities tend to be structured on a three-year term, if with annual renewal/extension options sometimes available.

Overall asset cover efficiency: Higher asset cover ratios tend to apply in sizing the unencumbered asset pool rather than would otherwise be expected on charged security.

We have advised on £540m of unsecured facilities in the past 12 months, and in several instances, facilities have been scaled up with the additional funding available in less than three weeks from the initial request.

Who should be thinking about it?

Funders will, of course, make decisions on a case-by-case basis, but in our experience, it is likely that an RP with the following would potentially benefit from this financing route:

Reasonable scale: lenders have a strong preference to be one among many lenders, which favours larger treasury portfolios

A strong credit profile – potentially supported by an external rating with a rating agency

A diverse loan portfolio, which is looking to ‘right size’ liquidity, while baking in flexibility and the ability to scale dynamically if needed

A big enough pool of residual unencumbered assets seeking to ‘sweat their assets’ more efficiently

The providers

While initially led by some of the newer entrants looking to make a footprint, most commercial funders will now entertain the prospect for the right RP.

In debt capital markets, some institutional investors have also demonstrated their ability and willingness to provide unsecured finance where suitably compensated in the spread, but experience informs us that this tends to be reserved for some of the larger RPs.

If debt capital markets funding is likely to be drawn, the cost differential can also be wider than seen on standby liquidity lines.

This is not to say there isn’t value in unsecured debt capital issuance, particularly where a portfolio contains challenging or quirky assets that would otherwise be challenging to leverage.

The increasingly challenging operating environment may dampen the appetite for unsecured lending among banking institutions, particularly should there be a general reduction in the sector’s credit standing.

However, for the time being we continue to see term sheets offering attractive unsecured funding from a broad range of lenders on a regular basis.

On that basis we consider this a viable solution that deserves due consideration in RP business plans across the country.

Gary Grigor, Partner at Devonshires, and John Tattersall, Senior Director at Centrus. Originally published in Social Housing Magazine, 2022.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you agree to our Privacy Policy

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.