Tuesday, Wednesdays and Thursdays (awkward acronym)?

How long for?

How will I be measured?

What is expected of a new joiner?

On a practical working and living level this uncertainty about the expectations of your role is unnerving. It impacts your decision making at many stages of your life and your career.

At Centrus there is no day that we are not grateful to work in roles that can be done from different locations. Employer and Employee earned the mutual trust to do this to a high standard during the pandemic, but we swiftly recognised that clarity on the working model as well as backing it up with committed policy and expectations was a very important next step.

What is NETworking?

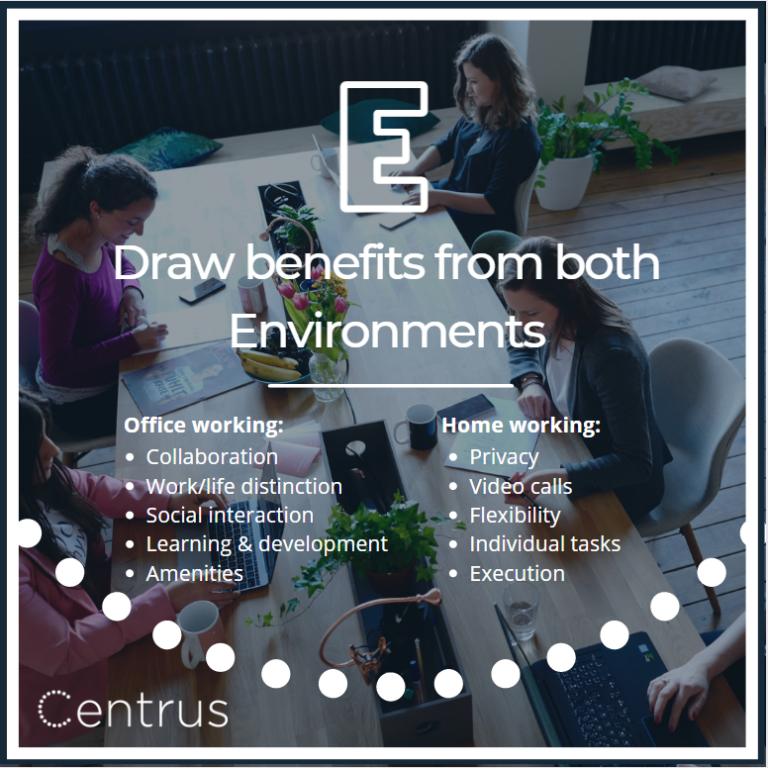

Everyone is in a different situation and motivated by different factors. To respect this, through team input, feedback and trial we established Centrus NETworking:

Needs – Client, Group, Team, Role and Personal

Environment – different types of work suits different working environments

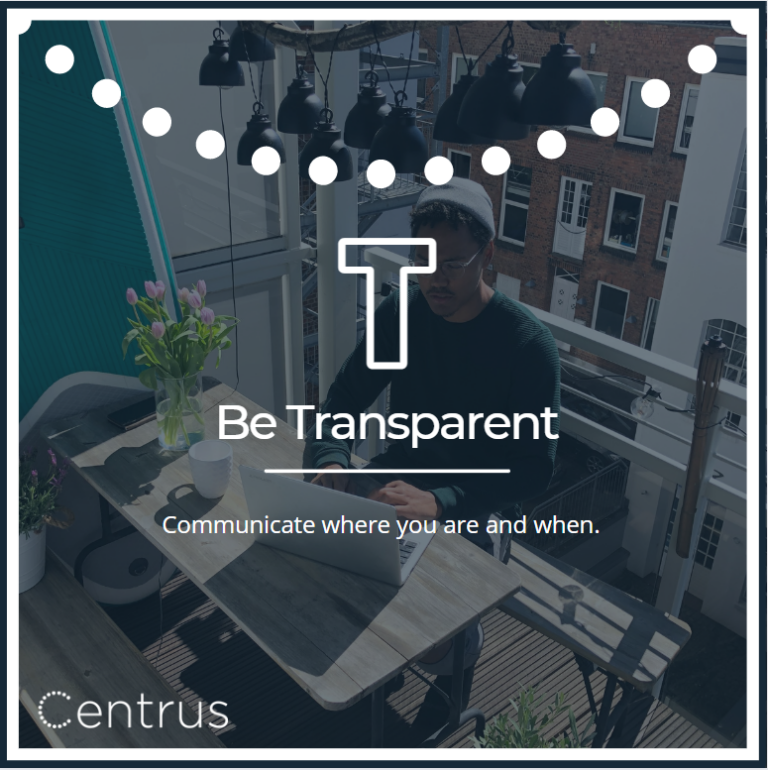

Transparency – Over communicate on where you are and where you will be

If you ever want to talk on our lessons learned or any other internal operational processes at Centrus please do get in touch with George Roffey, Chief Sustainability and People Officer at Centrus.

Risk and reward sharing is needed for housing association partnerships to work

Housing Associations (HAs) in the UK dominate the social and affordable housing sector, owning and operating a majority of the existing affordable housing stock. Most HAs are non-profit organisations where any income surplus generated is typically reinvested into the system to deliver more new affordable homes, capex or service debt.

The development of new affordable stock has not kept pace with the demand to the extent that latest estimates suggest a waiting list in excess of 1.2 million households in England alone. From a supply side perspective, the 10-year average from 2011/12 to 2020/21 has been 50,000 new affordable homes per annum which experts believe will need to increase three-fold to a total of circa 145,000 new homes per annum to meet demand. This poses a serious challenge for the HAs which are also facing sector-specific problems.

Headwinds and inherent constraints

HAs are faced with headwinds from essential fire safety upgrades in the near-term and large-scale decarbonisation expenditures required to meet net-zero targets in the more medium to long-term. Non-discretionary pressures on spend (which have no mitigation by way of increased revenues), heavy reliance on debt funding, constrained new debt capacity and a lack of equity inhibit HAs’ capacity and appetite for increasing development. Regulation, ratings pressures and lack of access to more subsidy or direct equity-raising capability add to the problem.

The case for private capital partnerships

Institutional funding has existed in the affordable housing sector for a long time in the form of long-dated debt investments. Given the rise of residential as an asset class in the UK and western Europe following the pandemic and the success story of institutional investment into student accommodation and build-to-rent in the UK, it was always a matter of time before the same institutions started to look at affordable housing sector through the equity lens.

Aside from diversification, the asset class is viewed to offer attractive risk-adjusted returns given low correlation to economic cycles and inflation-linked income. A spectrum of private capital providers are showing interest, with more real estate private equity style capital looking for higher risk reward via developments and quick aggregation play to deliver scale in a relatively short timeframe (3-5 years), whereas pension money backed capital view investments with a longer hold horizon and tend to be more focused on the stable income characteristics mainly driven by the need for matching pension liabilities.

Alternative capital solutions

A range of innovative capital solutions are at play and more are being developed as the sector draws further attention from institutional capital. Direct investment from institutionally owned for-profit registered providers (FPRPs), joint ventures applying forward purchase or forward funding, structured leases, fund structures as well as development joint ventures are either being implemented or developed. It’s fair to say that limited evidence exists to date but anecdotally a number of our HA clients have received enquiries and are working with us to receive independent advice and support in defining their financing objectives and identifying the most appropriate solutions to meet these.

Unlock additional affordable housing supply – the key attraction for the investor community is not only the steep supply-demand imbalance and long-term, stable income but also a sense of positive social impact that this investment class falls squarely into. The very strong ESG characteristics of this subsector are a major attraction for pension money, which is investing on behalf of stakeholders to build new affordable housing at the most impactful end of the scale.

Risk, reward and alignment

The key to this marriage lies in fair and transparent risk and reward sharing. Equally, alignment across both risk and reward as well as due consideration for the core purpose of HAs which is addressing the needs of underserved communities is absolutely key. In discussions with our HA clients this is an area of real focus and cultural alignment is as important as commercial and financial alignment.

There is an increasingly important role for equity in the affordable housing sector. However, it is down to individual HAs to assess their strategic objectives and goals first to work out the best possible application of equity and where this fits in the context of their current capital structure. We are working with a growing number of clients to support their strategies in this area providing independent advice to help them navigate a new and developing market and leveraging our unparalleled knowledge of the sector, capital markets and ratings agencies as well as equity investors.

Omer Fazal, Senior Director, Head of Real Estate – Centrus. Originally published in React News, May 2022

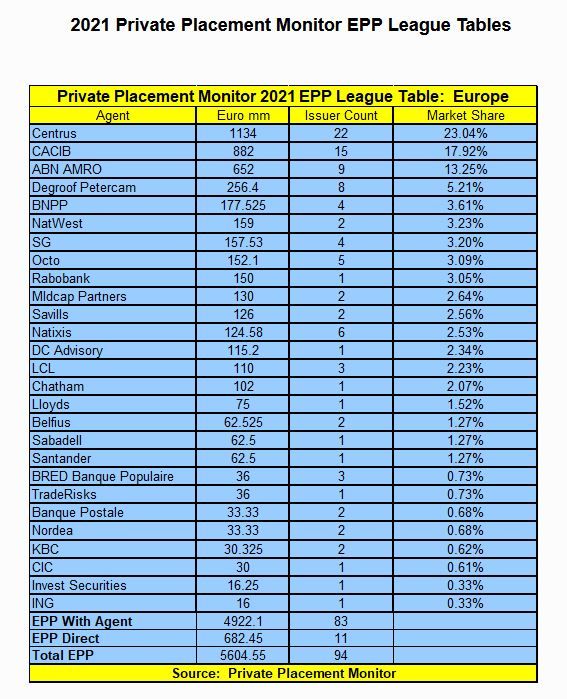

We are pleased to announce that Centrus has been ranked #1 on the Private Placement Monitor European Private Placement League Table by both deal count and volume for 2021.

To learn more about our work in this area with clients including London School of Economics, South Staffordshire PlC, Henderson European Focus Trust and Melin, click here.

For more information, please contact Maria Goroh, Senior Director – Centrus

Back in 2014, Centrus worked with Cross Key Homes to secure the first Housing Association issued ‘Green Bond’. Since then, we have been pleasantly surprised at the rapid adoption of Environmental, Social and Governance (ESG) accredited and labelled financing in the market. Between early 2020 and mid 2021, the housing sector moved from nearly 100% non-labelled issuance to 100% ESG labelled issuance.

While it is not yet a prerequisite for funding, ESG has become increasingly baked into the ecosystem, both for issuers building this into their reporting standards, as well as on the lender and investor side of the equation where it’s becoming fundamental to the credit process.

At this year’s NHF Housing Finance Conference Centrus Co-founder, Phil Jenkins and Director Lawrence Gill addressed the impact of ESG on the funding landscape. Centrus were joined by Anne Costain, Executive Director of Finance at Stonewater, Brenden Sarsfield Chief Executive Office at Sustainability for Housing and Imran Mubeen, Head of Treasury at Bromford Housing Group.

Here are three key takeaways from their discussion:

1. The Rise of ESG Reporting

The most immediate trend has been the rapid adoption of the Sustainability Reporting Standard (SRS). Launched in 2020, the SRS is a voluntary reporting framework, covering 48 criteria across ESG considerations such as zero carbon targets, affordability, safety and resident voice. With over 100 organisations signed up already, the sector has made a great start in adopting ESG reporting, which many believe will become mandatory in the future.

The SRS allows housing providers to report their ESG performance in a transparent, clear and comparable way. Not only does this differentiate the issuer from their competitors, but makes it easier for lenders and investors to assess ESG performance, risks and pursue opportunities.

Beyond the SRS, the next step could be to consider impact reports from an accredited third party. This will allow HAs to quantify how much benefit their actions bring and demonstrate with more clarity how they are generating positive change for otherwise underserved stakeholders.

2. The move towards Sustainability-Linked Bonds in the Housing Sector

While a Sustainability Bond, otherwise known as a ‘use of proceeds bond’, involves proceeds being allocated to projects which further the UN’s Sustainability Development Goals (SDGs), a Sustainability-Linked Bond (SLB) has Key Performance Indicators (KPIs) embedded within it. These are specific social and environmental targets aligned both to your sustainability strategy and the SDGs.

Earlier this year, L&Q successfully completed the first Sustainability-Linked Bond in the housing sector. The £300m issue directly linked to the housing association achieving a set of targets around reducing operational carbon emissions, improving the energy efficiency of residents’ homes, and delivering new affordable homes.

As Housing Associations are in intrinsically tied to ESG due to their responsibilities within communities in which they work, this is a clear next step for the sector.

3. More ambitious KPIs and goals

As the use of ESG labelled finance and SLBs become more widely adopted, and the sector inevitably opens itself up to criticism and accusations of greenwashing, the next challenge will be to ensure that these KPIs are set appropriately, transparently and that targets are sufficiently ambitious.

Targets should be about additionality – delivering benefits over and above the borrower’s business-as-usual strategy.

Relevant to the issuer’s overall business, and of high strategic significance to the issuer’s current and/or future operations

Measurable or quantifiable on a consistent methodological basis

Externally Verifiable, and

Able to be benchmarked, as much as possible using an external reference or definitions to facilitate the assessment of the organisation’s level of ambition.

Please get in touch with a member of our team for more information.

A race against time this Christmas as the GBP LIBOR cessation date approaches

The writing has been on the wall for LIBOR since 2017 when Andrew Bailey as head of the FCA declared that it would cease to be published and the market should transition to other more robust reference interest rates. However, some corporate treasurers and their relationship banks are now in a race to ensure certainty for their legacy LIBOR-referencing loan and derivative facilities ahead of the GBP LIBOR cessation date on 31st December 2021.

Facilities with GBP LIBOR fixings after 31st December face an uncertain future. The FCA has introduced “synthetic LIBOR” to be used in many of these facilities until 31st December 2022 to prevent widespread market disruption caused by LIBOR cessation. However, relying on this quick fix may not be in a borrower’s interest and the position for these facilities beyond 2022 is unknown.

Our own experience working with clients is that the volume of work has presented issues for many of the banks. However, the majority of lenders do now have a clear strategy and set of documentation which is capable of being entered into with no or very limited negotiation, so the remaining issues are very much practical rather than strategic.

How do you ensure certainty for legacy LIBOR-referencing loan and derivative facilities?

Treasurers can mitigate this uncertainty by actively transitioning their facilities to reference another interest rate, such as SONIA, or by ensuring their documents have robust fallbacks. Centrus has worked with many corporates and investors to actively transition their portfolios ahead of the cessation date.

For many clients that has involved a limited number of counterparties and facility agreements, frequently fewer than half a dozen and limited to cash products (loans). But to give an example of a larger portfolio, we recently supported Mitchells & Butlers plc with the transition of its £1.6bn whole business securitisation platform and related derivatives.

This process included the consent solicitation for all noteholders across the structure and resulted in the successful transition of its GBP and USD Floating Rate Notes to SONIA and SOFR respectively.

In addition, we are working with other corporates across the regulated utilities, economic infrastructure and real estate sectors to transition their facilities at an operating entity level, including a vast portfolio of project companies managed by Equitix Limited.

If you are finding LIBOR transition to be the Nightmare Before Christmas, don’t hesitate to contact the Centrus team to see how we can support you and ensure that you have a Wonderful Christmastime.

There has been plenty written now on the LIBOR/SONIA transition and the methodology is becoming clear, albeit undoubtedly more complicated than originally envisaged. The purpose of this client briefing note is to offer some comments on calculation methodologies, discuss operational implications and explain how a treasury management system can help you through the transition. We also explain how the treasury management system we offer (titantreasury) can help from an operational perspective, for those clients where automation may be useful.

This note has been prompted by the passage of time since our last paper on LIBOR (which has more on the historical context) but also by the announcement on 5th March 2021 by the Financial Conduct Authority on “future cessation and loss of representativeness of the LIBOR benchmarks”. The operative clause for many readers in the UK will be the statement:

“Immediately after 31 December 2021 …1-month, 3-month and 6-month sterling LIBOR settings will no longer be representative and representativeness will not be restored.”

This has two main effects in our view:

1) Confirmation that the policy remains on track. There are exceptions for USD LIBOR and likely to be provision to deal with genuine “tough legacy contracts” but for Sterling loans and derivatives the coffin has one fewer nail left not firmly hammered down.

2) It aligns with the framework set up by the International Swaps and Derivatives Association (“ISDA”) and it triggers the fixing of the Spread Adjustments which will apply for derivatives where parties have adopted the “ISDA Protocol”.

3) The Spread Adjustment for 3-month GBP LIBOR (for example) for relevant contracts is now set at 11.93 basis points. Corporates will often not be locked to these spread adjustments, even for derivatives, but they are gaining status as ‘benchmarks’.

Green Hydrogen is seen as the next key step in generating heating for homes and fuel for transport. Whilst it has been talked about as the ‘fuel of the future’ since the 19th century, its promise is starting to be realised thanks to falling costs and scope for curbing emissions. The UK Government’s Energy White Paper sets out a picture of how we aim to achieve net zero emissions by 2050, but key questions remain…

Is there appropriate infrastructure for hydrogen as a fuel for transport?

How will hydrogen get to our homes?

Can hydrogen be produced cost effectively?

What is the UK govt doing to help and is this support fit for purpose?

Is this sector interesting for private finance?

Chaired by Terence Amako, head of M&A at Centrus, we have an exciting list of panellists helping us to answer these questions; joining us is John Morea, CEO at Scotia Gas Networks (SGN), David Surplus, Managing Director at B9 Energy, Martin Bradley, MD at Macquarie, and Thomas Studer, Technology & Innovation at Macquarie.

Join us for the launch of the Sustainability Reporting Standard for Social Housing, an important development in unlocking the significant new private investment needed by the social housing sector.

The launch is the culmination of a 12 month process, initiated by the 17 sponsors and members of the ESG Social Housing Working Group and a consultation which has taken in the views of 250 organisations from across the social housing and financial sectors. We expect more than 60 housing associations, lenders and investors to commit being early adopters of the new Standard.

We’ve lined up some great speakers, including Bob Kerslake (Peabody), Harvey McGrath (Impact Investing Institute and Big Society Capital), Sarah Forster (The Good Economy), Phil Jenkins (Centrus), Paul Hackett (Optivo), Clare Miller (Clarion), Simon Century (LGIM), Natalie Elphicke (UK Parliament), and moderated by Merryn Somerset Webb (Moneyweek).

Please join us for what promises to be a lively and engaging discussion on the benefits of the new Standard.

Registered Providers are under huge pressure to increase spend on fire safety measures and de-carbonisation, whilst simultaneously struggling to support vulnerable tenants, rent arrears and deliver new housing supply. Leading you through this veritable minefield, will be Julian Ashby and Simon Dow, Previous and Interim Chairs of The Social Housing Regulator, expertly held in line by Phil Jenkins, MD of Centrus.

This webinar covered:

What to do in a time of recession; sacrifice development with uncertainty about the cross subsidy model, or land bank?

Should you fill your boots with cheap fixed interest debt or worry about negative inflation and an unsustainable rent formula?

Are money in the bank and development opportunities a winning formula for attracting merger partners or is low debt per unit the honey trap?

Walking the tightrope between delivery and staying on the right side of the Regulator and the Credit Rating Agencies?

“Covid adds new dynamics to stress testing; but it has also illustrated new ways of doing business and new ways of engaging with residents.”

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you agree to our Privacy Policy

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.